Paraguay tax residence vs. domicile

How Tax Residency in Paraguay Really Works

Understanding Paraguayan tax residency can feel like walking through a hall of mirrors. Some sources say you need 0 days, others say 90, 120, 180, 183 or even 200 days in the country. The result is confusion.

The reality is simpler. Paraguay does not impose any legal minimum-day requirement to be a tax resident.

Key points you should know

• There is no minimum-day rule in Paraguayan law for tax residency.

• The famous “120 days” rule refers to domicile, not tax residency

• Tax residency = which country has taxing rights over you.

• Domicile = your legal address inside the country.

• General Resolution 65/2020 governs the tax residency certificate and does not impose a day-count requirement.

• Maintaining tax residency depends on keeping your RUC compliant ("cumplimiento tributario") and preserving your immigration residency (not loosing it). By loosing immigration status (from whatever reason) you automatically loose tax residency.

1. The law

Two legal sources define the modern framework:

Law 125/1991

This is the backbone of Paraguay’s tax system. Crucially, it never introduced a minimum-day requirement for tax residency.

General resolution 65/2020

This resolution sets the current procedure for obtaining the tax residency certificate.

It defines the process, not a threshold of days.

Sources:

• Resolución General Nº 65/2020

What GR 65/2020 actually requires

GR 65/2020 does not states to "stay X days in Paraguay".

Specifies the procedural documents to obtain tax certificate, including:

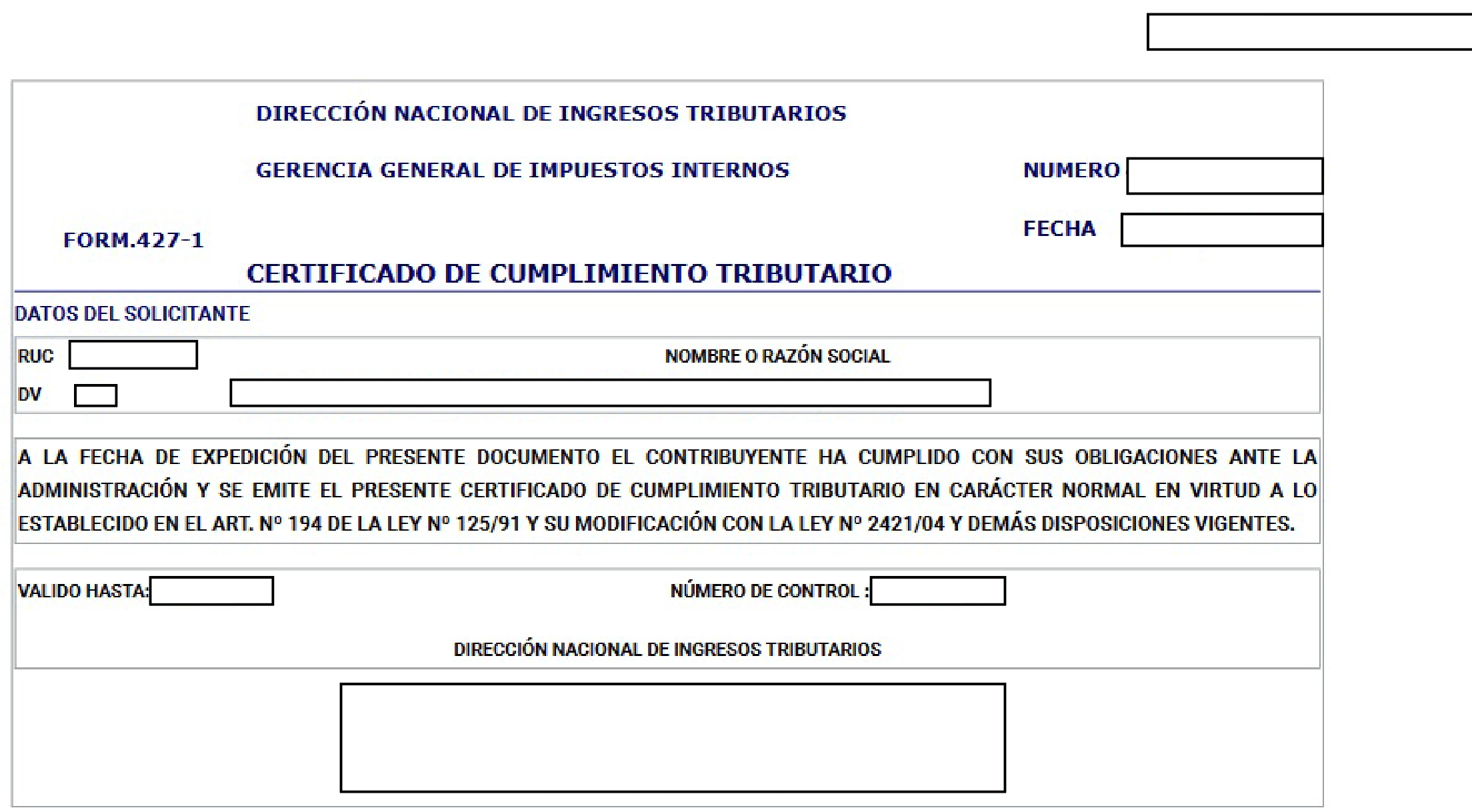

1. Certificado de Cumplimiento Tributario

- Confirms your RUC (taxpayer ID) is up to date with all filings.

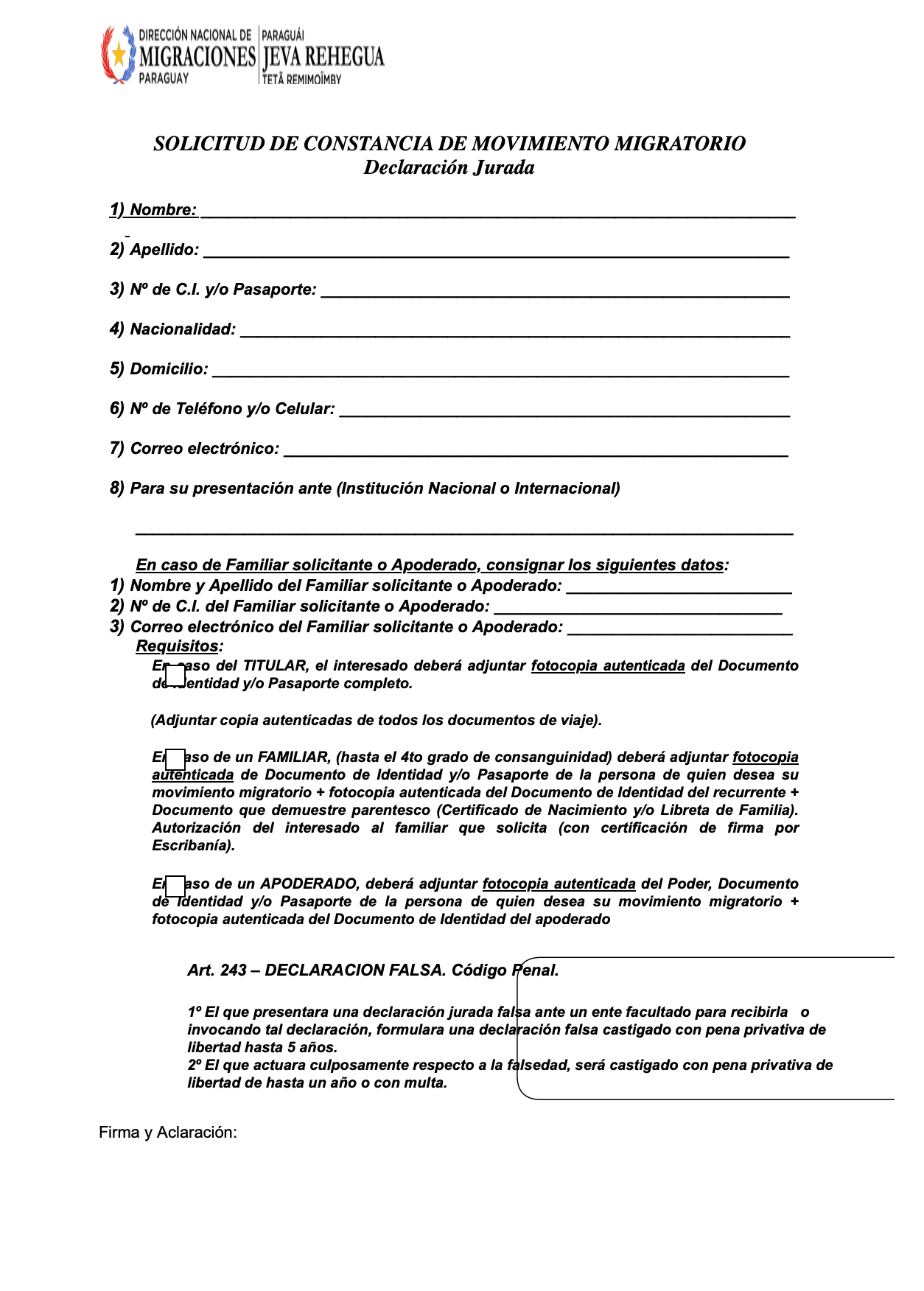

2. Constancia de Movimiento Migratorio

- A migration report listing all entries and exits. Available via: Portal Paraguay

3. Have a RUC number

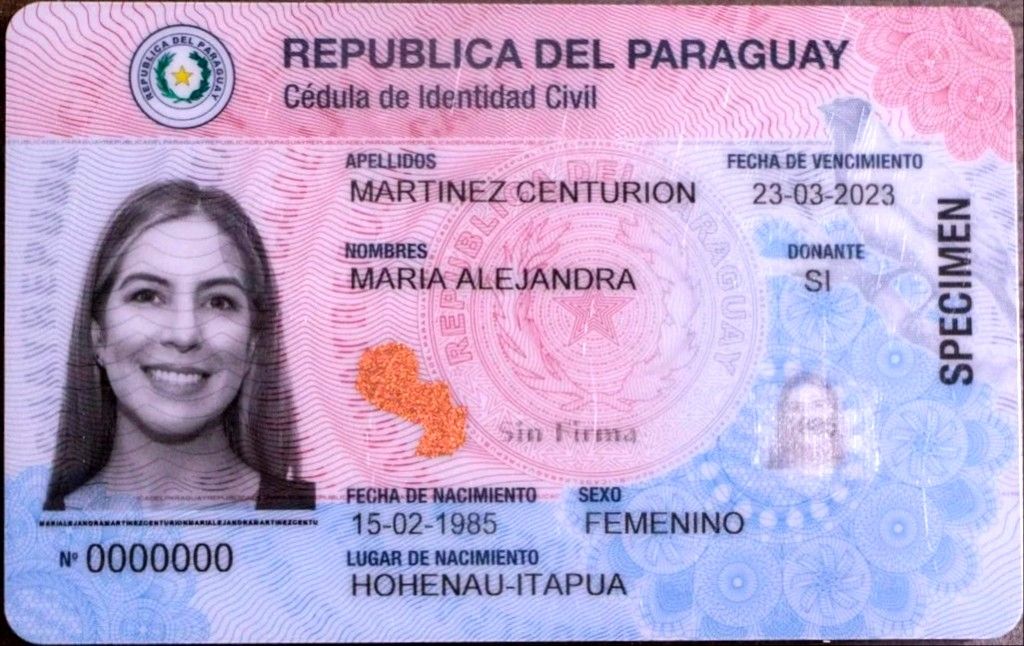

4. Present valid cédula

Article 3 in GR 65/2020 specifies this below:

Example

A software consultant living among 3 countries (Thailand, Portugal, Colombia) and visits Paraguay twice a year for two weeks.

He:

• maintains a RUC

• files relevant taxes

• provides the migration record

• complies with GR 65/2020

He receives the tax residency certificate, no day-count discussion.

In practice: Will DNIT deny a certificate because he spent “not enough days”? No. DNIT focuses instead on whether his RUC is compliant, his filings make sense, and his fiscal activities are consistent.

2. The 120-day rule (what it is)

Many people are spreading rumors that “120 days = automatic tax residency”

There is often confusion between tax residency and tax domicile.

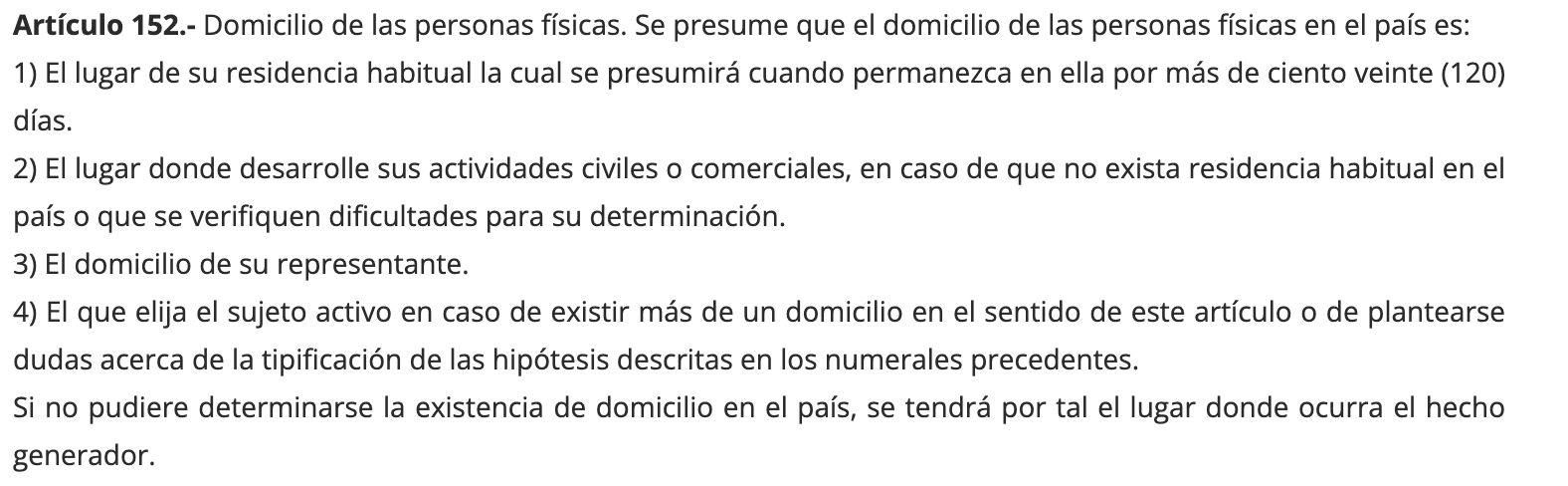

What article 152 actually says

Paraguay presumes a person’s domicile to be:

- The address where a person habitually lives when they spend more than 120 days there.

- The location where they carry out their civil or business activities, if their usual residence is unclear or cannot be established.

- The official address of their legal representative.

- A domicile selected by the taxpayer when there is more than one possible option or when uncertainty exists about which applies.

- If no domicile in Paraguay can be identified through the previous criteria, the address is taken to be the place where the taxable event occurred.

The 120-day clause creates a presumption of habitual residence, nothing more.

It does not create a minimum-day requirement for tax residency.

Example: Why the distinction matters

A person may spend only 20 days in Paraguay but:

• carry out their business activities through a local entity

• register a domicile with representative

• maintain a compliant RUC filing

• file taxes in Paraguay

This person can be domiciled and tax resident without being 120 days in the territory.

If you spend more than 120 days your domicile is presumed to be the place where you stayed.

If you spend less than 120 days your domicile is determined through one of the alternative options(activities, representative, elected domicile).

Sources:

• Ley Nº 125/1991 – Régimen Tributario

3. What you need to have in order

The absence of a days in the territory requirement does not mean “you do not have to do anything.”

Your position must be defensible.

You must:

• Maintain a valid RUC

• File and pay taxes according to your economic activity

• Follow GR 65/2020 requirements

• Align your documentation with one of the domicile options

• Maintain your physical immigration residency. If you lose your temporary or permanent residency (e.g., failing to visit Paraguay every 12 months as temporary resident or 36 months as a permanent resident), you automatically lose tax residency as well.

Why domicile services are legally valid

Because Article 152 explicitly recognizes:

• domicile via a representative

• domicile chosen by the taxpayer

This makes services such as professionally-managed proof of domicile via attorney office perfectly compatible with Paraguayan law even when your physical stays are limited.

Takeaway

Paraguay’s tax residency rules are remarkably straightforward:

• No legal minimum-day requirement exists.

• The “120-day rule” is a misunderstanding of topics domicile vs. tax residency

• GR 65/2020 defines the procedure what to comply with.

• Your tax residency depends on RUC compliance, proper handled documentation, and maintaining your immigration status valid.